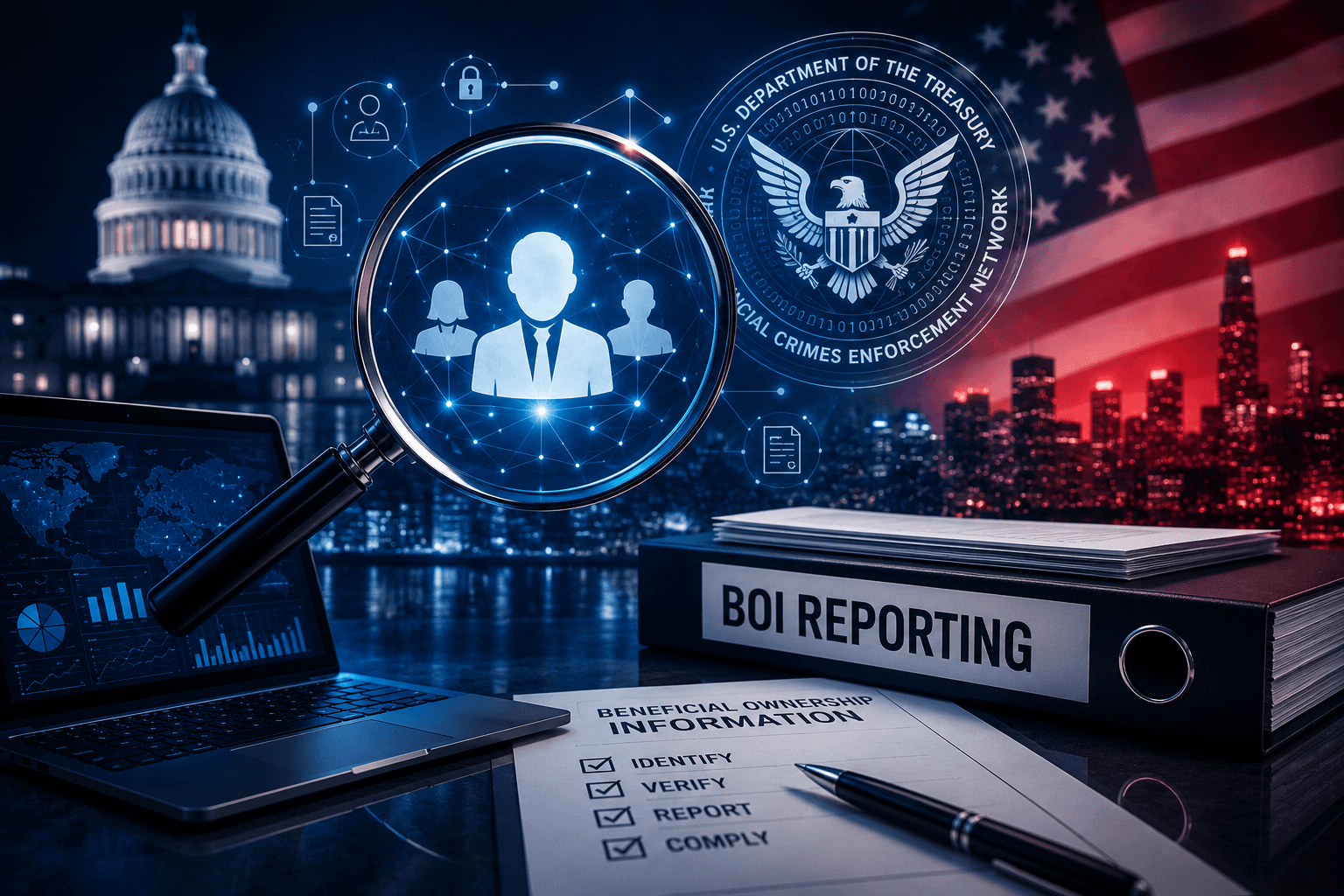

Beneficial Ownership Information (BOI) Report

The U.S. Corporate Transparency Act (CTA) was enacted as part of the Anti-Money Laundering Act of 2020. The law imposes a new federal reporting obligation on certain entities in the United States and outside the United States – the Beneficial Ownership Information (BOI) report. As part of the BOI report, information about the entity’s beneficial owners must be submitted to the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury.

This article explains who is required to file a BOI report, what information must be included in it, and the filing deadlines that apply to this reporting requirement

Why was the BOI reporting law enacted?

U.S. entities with foreign shareholders (for example, a U.S. entity owned by Israelis) are often considered “reporting companies,” even if they have no physical operations in the United States. BOI reporting is separate from reports submitted to the Internal Revenue Service (IRS), and it creates a national registry of beneficial ownership to enhance financial transparency. Compliance with the requirements includes identifying beneficial owners, collecting relevant documents, and meeting reporting deadlines. Ultimately, the purpose of the legislation is to combat money laundering, terrorist financing, and the misuse of shell companies.

Who is required to file a BOI report?

The U.S. Corporate Transparency Act adopted the term “reporting companies,” which, in the legislative context, refers to entities that were formed or registered to do business in the United States by filing with a Secretary of State or a similar authority. This framework generally includes two main categories of entities that are required to file BOI reports:

- Domestic companies – corporations, limited liability companies (LLCs), and other entities formed under the laws of a U.S. state by filing formation documents.

- Foreign companies – non-U.S. entities that have registered to do business in a U.S. state.

Most small privately held companies, startups, family businesses, and foreign-owned U.S. entities are required to file. However, the law includes more than twenty exemptions, primarily for entities that are already subject to extensive federal or state supervision. Common exemptions include public companies, banks and credit unions, insurance companies, investment companies and registered investment advisers, as well as large operating companies with more than 20 full-time employees in the United States, more than USD 5 million in gross receipts in the United States, and a physical office in the United States.

Who is a beneficial owner?

A beneficial owner is any individual who, directly or indirectly, owns or controls at least 25% of the ownership interests in a company, or who exercises substantial control over the company. For this purpose, “substantial control” applies to individuals serving as senior officers, such as a CEO or CFO, individuals with authority to appoint or remove senior officers or directors, or individuals who direct important business decisions.

In practice, this means that BOI reporting is not limited to shareholders. Managers, controlling members, and certain decision-making role holders may also be considered beneficial owners who must be reported.

In addition, companies formed on January 1, 2024, or later must also report their company applicants, meaning the person who filed the formation document and, in certain cases, the person who directed the filing process.

What information must be included in the report?

BOI reports are filed electronically with FinCEN through a dedicated system, and they are not available for public inspection. In general, the report includes information about the company, such as its legal name, trade name, business address, state or country of formation, and IRS taxpayer identification number. In addition, the relevant company must provide information about each beneficial owner, such as full legal name, date of birth, residential address, and the number and image of an identification document.

Important filing deadlines

As of 2026, the filing deadlines for BOI reports depend on the date on which the reporting company was formed or registered, and filings are made through FinCEN’s electronic BOI reporting system. For the most up-to-date deadlines and additional updates, click here.

Penalties

Failure to comply with BOI reporting requirements may result in fines of up to USD 500 per day. In addition, companies may be exposed to criminal penalties of up to USD 10,000 and up to two years of imprisonment.

BOI reporting has now become a significant reporting obligation in the United States, and the filing process and the documents required for it demand attention and accuracy. Our firm specializes in U.S. taxation, and we would be pleased to assist you with the BOI reporting procedures required for you.

TaxLink – Our Story

TaxLink is a Certified Public Accounting (CPA) firm specializing in both U.S. and Israeli taxation. Our practical experience with the Internal Revenue Service (IRS) and the Israel Tax Authority, combined with a deep understanding of the interaction between the two systems, allows us to build a tailored end-to-end solution for your case.

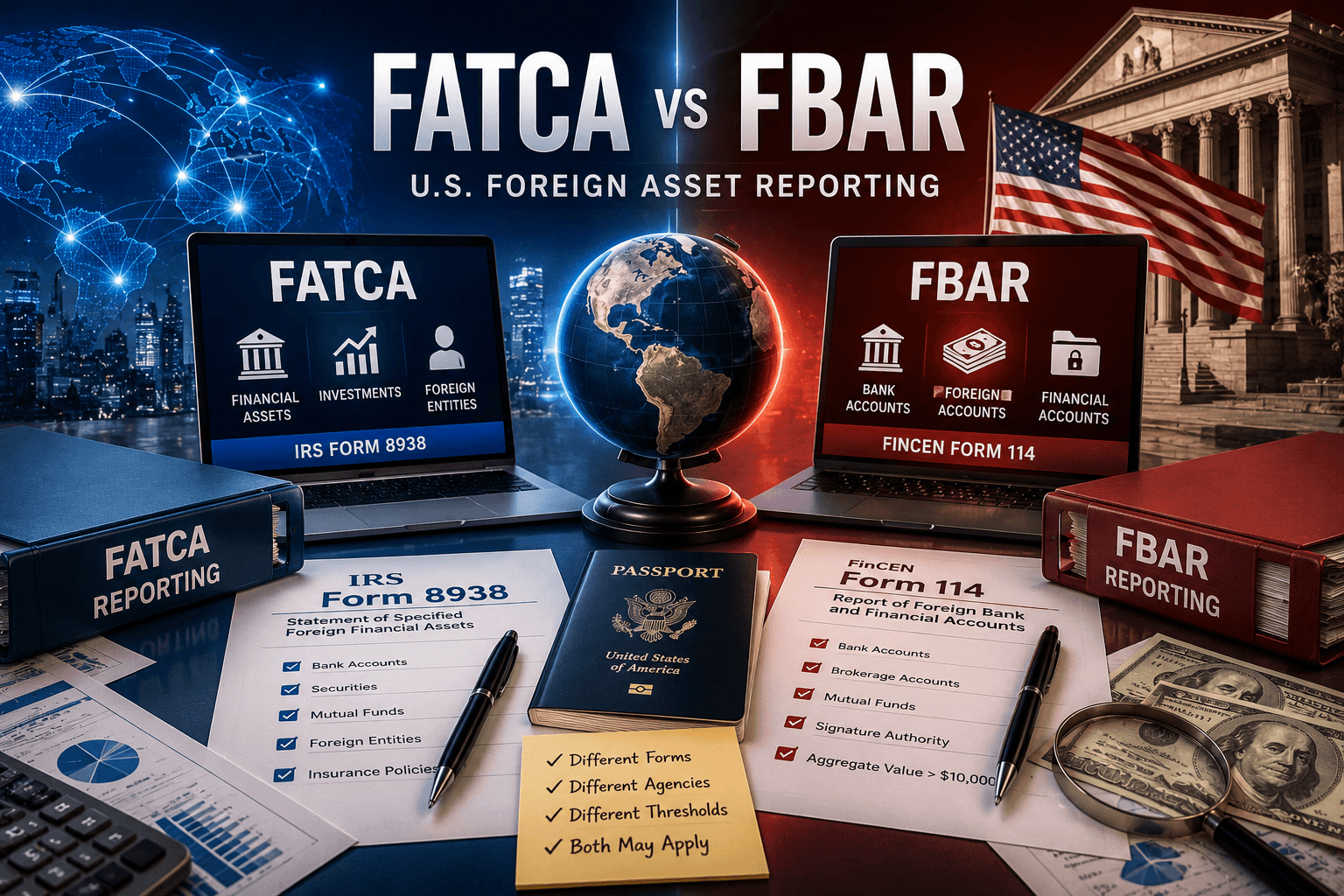

Most clients who contact us do so because they are required to file reports in the United States – whether a Form 1040, Foreign Account Tax Compliance Act (FATCA) reports, Foreign Bank Account Report (FBAR) filings, or reports relating to real estate investments in the United States. We manage the process as a coordinated cross-border matter, with the aim of reducing errors, avoiding duplication, and helping to prevent double taxation, all within the framework of U.S. law, Israeli law, and the tax treaty between the United States and Israel.

Frequently Asked Questions

What is a BOI report under the Corporate Transparency Act?

A BOI report is an electronic filing submitted to FinCEN that identifies the reporting company and certain individuals who own or control it.

Which companies are generally required to file a BOI report?

Many entities formed by filing with the company registry in a U.S. state, or with a similar authority, as well as many foreign entities registered to do business in the United States, may be considered reporting companies unless an exemption applies.

Are BOI reports public or searchable?

No. BOI reports are not available for public inspection, although FinCEN may disclose them to authorized parties in limited circumstances.

Does BOI reporting replace any reports to the Internal Revenue Service?

No. BOI reporting is separate from federal and state tax filings and does not replace any other reporting obligation to the IRS.