U.S. Real Estate Investors

Tax-Link » U.S. Real Estate Investors

Do you own a U.S. investment property? Here’s how to handle reporting and taxation in both the U.S. and Israel efficiently, in an organized way, and without surprises.

Roadmap:

How to report a U.S. real estate investment - step by step

Obtaining a U.S. taxpayer identification number

The first step in the process is to make sure you have a taxpayer identification number for U.S. filing and tax payment purposes. If you are an Israeli resident who is not a U.S. citizen or U.S. resident, you will need to obtain an ITIN (Individual Taxpayer Identification Number). Alternatively, U.S. citizens and certain U.S. visa holders have an SSN (Social Security Number), which they can use to file.

An ITIN is obtained by filing Form W-7 together with certified identity documents and supporting documentation (for example, a tax return, a lease agreement, or a withholding agent letter).

With us, you can obtain your ITIN through a certified agent whose role is to verify your identity and handle the ITIN application on your behalf, helping you avoid complex procedures. Keep in mind that ITIN processing typically takes 8-12 weeks.

Choosing a tax treatment for rental income

Under the default rules, a foreign person who is not a U.S. resident is taxed on U.S. rental income at a rate of 30% on the gross rental income. As part of this, you will be required to provide the payor/withholding agent with Form W-8BEN, and in return you will receive Form 1042-S at year-end.

Alternatively, you may elect to treat U.S. rental income as Effectively Connected Income (ECI). This classification allows you to deduct allowable expenses (including depreciation and permitted financing costs) and may, in some cases, significantly reduce your overall tax liability. In practice, you provide the withholding agent with Form W-8ECI and make the election on your first Form 1040-NR. This election remains in effect until you revoke it.

The annual U.S. tax return

The annual U.S. tax return (for a taxpayer who is not a U.S. citizen or U.S. resident)

On Form 1040-NR, you will report income from your U.S. real estate investment and the allowable expenses (management fees, repairs, insurance, municipal taxes, property tax, interest expense, and depreciation). If tax was withheld at source, Form 1042-S should be attached. The common filing deadline for taxpayers living outside the U.S. is June 15 (an extension is generally available). Note that paying any tax by the deadline helps avoid interest and penalties.

State tax return

In some cases, you may also be required to file a state tax return in the state where the property is located. Some states impose state-level income tax and require a separate return (for example, New York and California), while other states do not impose individual income tax (for example, Texas and Florida). Tax rules, including deductible expenses, depreciation, and credits, vary from state to state.

Filing an Israeli tax return

In Israel, you generally have two alternatives for reporting rental income from the U.S.:

(a) A 15% tax track - under this track, only depreciation expenses may be deducted, and no credit is allowed for foreign taxes paid in the U.S.;

(b) A regular tax track under the marginal tax brackets - under this track, you report net income after deducting all expenses incurred to produce the income (including, for example, financing costs and depreciation subject to the rules), and you may claim a credit for foreign taxes paid in the U.S., subject to the foreign tax credit rules.

In any event, under both tracks - and unlike the simplified track available for Israeli-source rental income - you are required to file an annual tax return (Form 1301) in Israel.

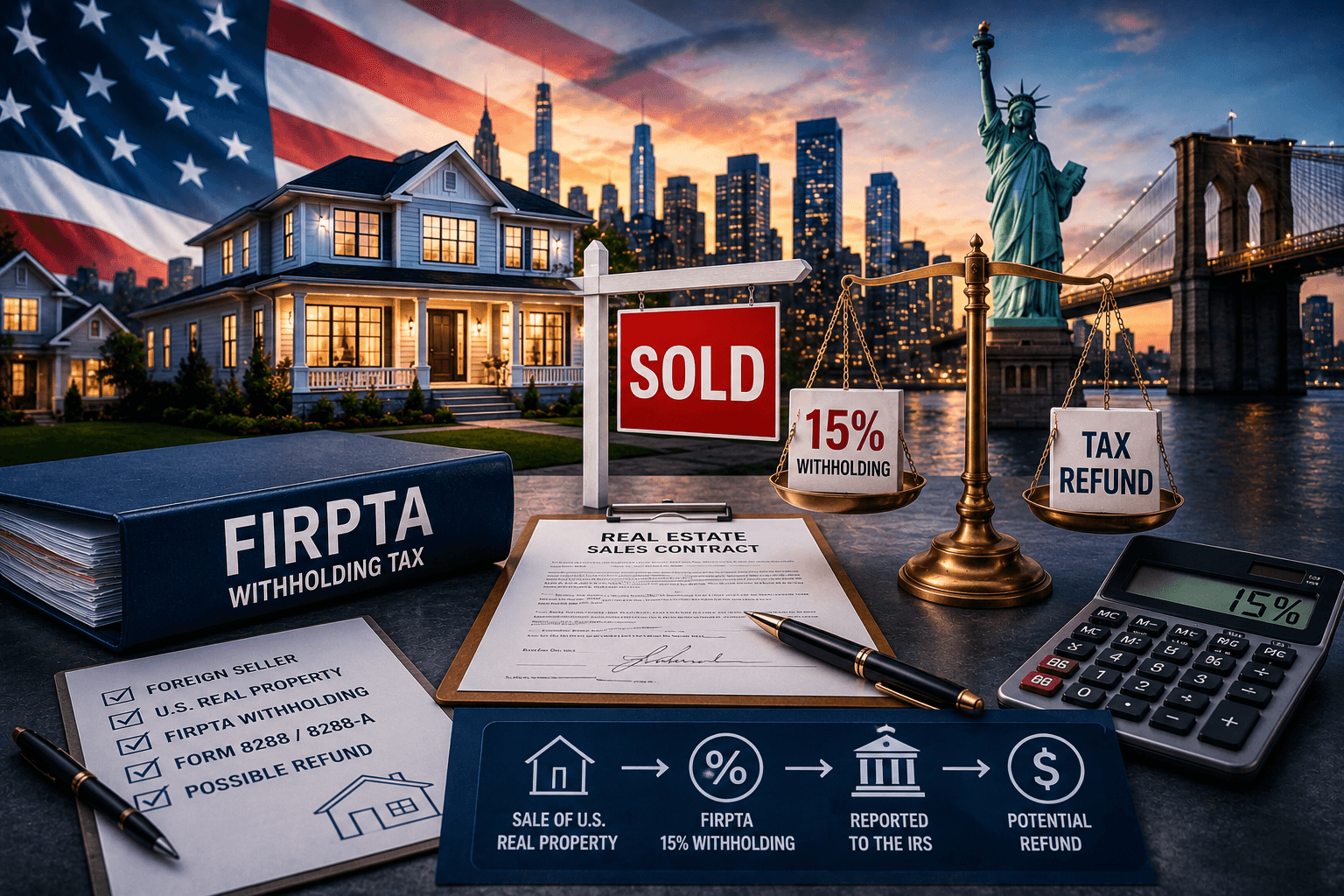

FIRPTA in the U.S. and filing an Israeli tax return

Upon sale of the property, U.S. tax will apply under the Foreign Investment in Real Property Tax Act (FIRPTA). This is a U.S. tax regime that applies to foreign investors selling U.S. real estate. The tax is collected through withholding at source at a rate of 15% of the gross sales proceeds, unless a reduction or exemption is obtained in advance. The final tax is reported on Form 1040-NR based on the net capital gain, with a refund of any excess withholding.

Of course, in addition to the U.S. filings, you will also be required to report the sale of the property in Israel, while claiming a credit for foreign taxes paid in the U.S. (federal and state).

How we at Tax Link

Can help you with U.S. real estate investments

- End-to-end guidance and handling of all reporting obligations related to your U.S. real estate investment, including:

- Full assistance with obtaining an ITIN;

- Reviewing the optimal tax treatment (ECI versus 30% withholding under the default rules);

- Assistance in completing Forms W-8BEN or W-8ECI, as applicable;

- Preparation and filing of Form 1040-NR, state tax returns (if required), and FIRPTA filings upon sale;

- Filing your Israeli tax return, including the required adjustments under Israeli tax law, and reviewing the optimal Israeli tax track for you.

Key U.S. filing deadlines

- ITIN issuance: It is recommended to apply as early as possible before renting out the U.S. property. Keep in mind that ITIN issuance can take time, so it is best to plan ahead and apply early.

- Form 1040-NR: Generally due on June 15 of the following year, with an extension option in certain cases up to October 15.

- State tax return: If a state tax return is required, the filing deadline depends on the internal law of each state.

Articles and Guides

Investing in U.S. Real Estate: FIRPTA Withholding Tax

Foreign Investment in Real Property Tax Act – FIRPTA FIRPTA

Taxation of Ongoing U.S. Rental Income for Foreign Residents

Owning rental property in the U.S. can be a profitable

FAQ

Do I need to file with the IRS if I own U.S. real estate?

Yes. Israeli residents who own U.S. real estate generally need to file in the U.S. using Form 1040-NR.

How do I file in the U.S. if I own U.S. real estate?

To file in the U.S., Israeli residents who are not U.S. taxpayers must obtain a U.S. taxpayer identification number (ITIN – Individual Taxpayer Identification Number) and file using Form 1040-NR. In many cases, you will also need to file a return in the state where the property is located.

How do you obtain an ITIN?

You obtain an ITIN by filing Form W-7. The application must be accompanied by additional documents such as a valid passport, a U.S. visa (if applicable), the date of your most recent entry into the U.S., and the reason you are applying for the ITIN. As part of the process, an identity verification procedure is required, which can be completed through an authorized representative on our behalf.

What U.S. tax applies to rental income from the U.S.?

U.S. rental income earned by Israeli residents is subject to 30% withholding tax on gross rent, and the Israel-U.S. tax treaty does not reduce this rate. In Israel, additional tax may apply depending on the reporting track you choose.

What Israeli tax applies to rental income from the U.S.?

U.S. rental income may be taxed in Israel under one of two tracks: (a) the regular (marginal) tax track – income is taxed at your applicable marginal rate, with deductions for expenses incurred to generate the rental income and a credit for foreign taxes paid in the U.S.; or (b) a fixed 15% tax track with no expense deductions (other than depreciation) and no credit for U.S. tax.

Do U.S. real estate owners also need to file in the state where the property is located?

Often, real estate investors who own U.S. property must also file in the state where the property is located. The obligation depends on that state’s rules, including whether the state imposes state income tax, whether there were profits from the investment in that year, and other factors.

Why Choose Tax-Link?

One Stop Shop – US and Israeli tax reporting under one roof – no back-and-forth coordination between an Israeli CPA and a US CPA. End-to-end handling, all in one firm.

A personal approach – High-level professionalism alongside clear, pleasant communication. You always know exactly where things stand.

A clear process with minimal involvement on your part – Smart document collection, an organized workflow, and full end-to-end process management by our team.

Transparency and Fair Pricing – Real-time status updates, clear deadlines, and no surprises.