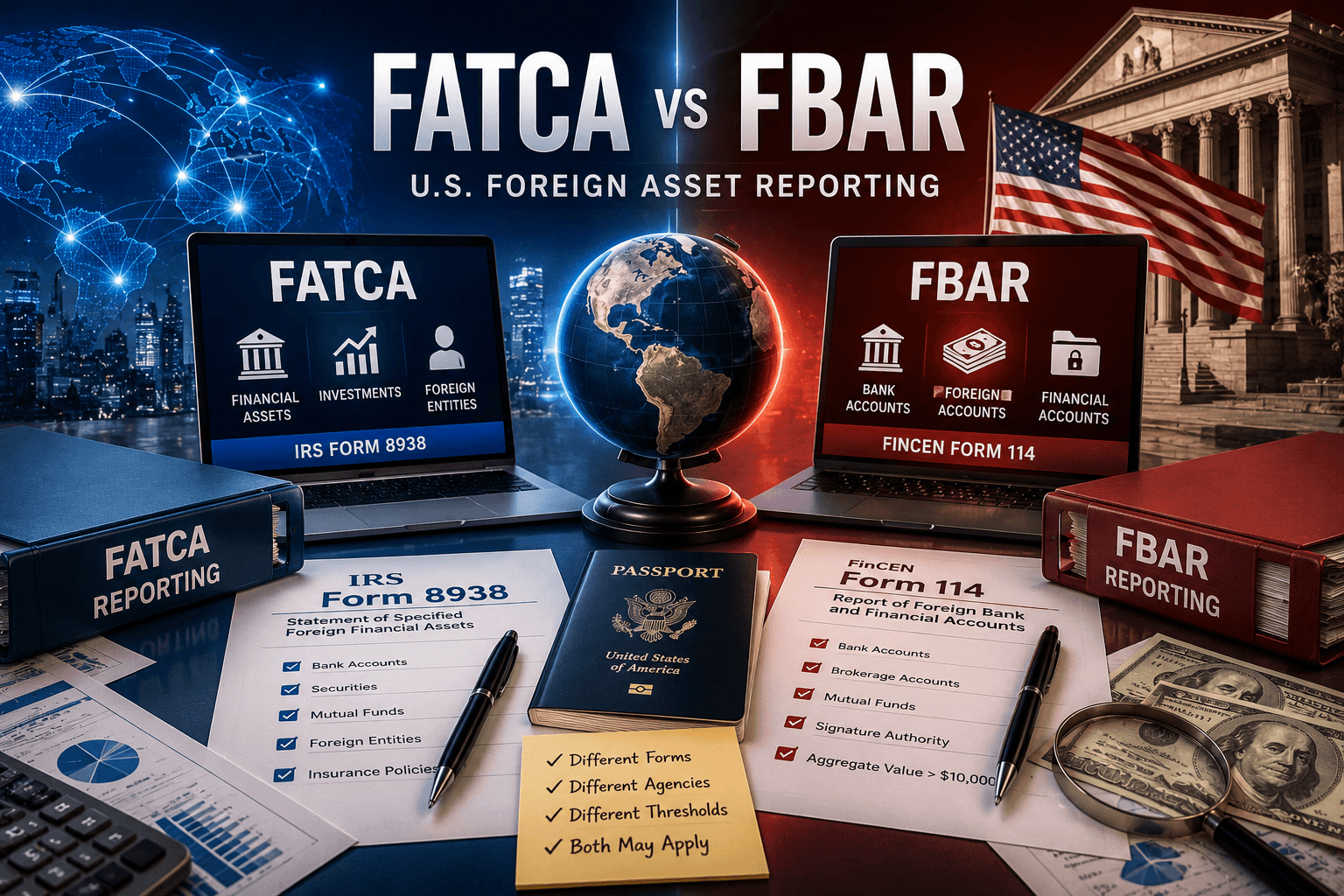

As cross-border financial activity grows, many U.S. citizens hold accounts and assets outside the United States. To promote transparency and prevent tax evasion, the U.S. government introduced two separate reporting regimes: the Foreign Account Tax Compliance Act (FATCA) and the Foreign Bank Account Report (FBAR)

U.S. Reporting Obligations for Foreign Assets

FATCA was enacted in 2010 to combat tax evasion through undeclared funds held in foreign accounts. In general, the law requires financial institutions outside the United States to provide information regarding assets held by U.S. citizens. In addition, U.S. taxpayers are required to report their foreign financial assets to the Internal Revenue Service (IRS) each year.

By contrast, there is another important reporting obligation: FBAR, which was established under U.S. banking laws. This obligation requires individuals and entities to report financial accounts held outside the United States each year. This includes bank accounts, brokerage accounts, and mutual fund accounts, if the aggregate amount exceeds a certain threshold.

FATCA and FBAR – Key Differences

Although FATCA and FBAR are both intended to combat tax evasion through assets held outside the United States, there are differences between them in terms of scope, reporting obligations, and the sanctions that may apply in the event of non-compliance. Key differences include:

- While FATCA matters are administered by the IRS, FBAR is overseen by the Financial Crimes Enforcement Network (FinCEN), which focuses on preventing money laundering and promoting financial transparency in order to prevent financial crimes.

- FATCA was originally designed to combat tax evasion through disclosure obligations imposed on U.S. taxpayers and foreign financial institutions, whereas FBAR is intended to monitor the use of foreign bank accounts, ensure transparency, and reduce misuse for tax evasion and/or money laundering purposes.

- FATCA applies to U.S. citizens and U.S. tax residents, as well as certain specified domestic entities, that hold specified foreign financial assets above certain thresholds. For individuals, the reporting threshold (for 2025) generally begins at $50,000 for certain single filers living in the United States, although the threshold varies depending on filing status and whether the taxpayer lives in or outside the United States. Different rules apply to certain specified domestic entities. By contrast, FBAR applies more broadly to a “U.S. person,” including U.S. citizens, green card holders, tax residents, and U.S. entities such as corporations, partnerships, and trusts. For those required to report, FBAR filing is generally required if they have a financial interest, economic connection, signature authority, or other authority over foreign financial accounts, and the aggregate value of the accounts exceeds $10,000 at any point during the year (for 2025). Filing one form does not replace the other when both reporting regimes apply.

- To comply with FATCA obligations, taxpayers are required to file IRS Form 8938 together with their annual tax return. By contrast, FBAR reporting is submitted through FinCEN Form 114 using an online system.

- FATCA obligations apply to a wider range of foreign financial assets, including bank accounts, shares, bonds, mutual funds, interests in foreign entities, and foreign insurance policies. FBAR, by contrast, focuses more specifically on foreign financial accounts, such as bank accounts, brokerage accounts, and mutual fund accounts.

- Non-compliance with FATCA may result in civil penalties starting at $10,000, which may increase up to $50,000 in the event of continued non-compliance after notice is provided. FBAR violations carry more severe sanctions: non-willful violations may result in a penalty of up to $10,000 per account, while willful violations may result in a penalty equal to the greater of $100,000 or 50% of the account balance.

- The initial FBAR filing deadline is April 15, while the FATCA filing deadline is the deadline applicable to the individual’s income tax return. If the FBAR is not filed by April 15, the filing deadline is automatically extended to October 15.

The following table provides a simplified comparison of the key differences between FATCA and FBAR:

FATCA | FBAR | |

Legislative source | Enacted in 2010 as part of the HIRE Act | Originates in the Bank Secrecy Act of 1970 |

Form number | IRS Form 8938 | FinCEN Form 114 (not an IRS form) |

Who is required to file | U.S. taxpayers (citizens, residents, and certain non-residents) with specified foreign assets | U.S. persons (citizens, residents, and entities) with foreign bank accounts |

Where it is filed | Filed together with the federal tax return (Form 1040) | Filed electronically with FinCEN, separately from the tax return |

Reporting threshold | Higher thresholds (for example: $50,000 for an individual / $100,000 for a couple at year-end for foreign assets) | Lower threshold: $10,000 in the aggregate across all foreign accounts |

Types of assets included | Broader: foreign bank accounts, shares, mutual funds, retirement accounts, and more | Narrower: only foreign financial accounts |

Purpose | Preventing tax evasion through foreign financial assets | Identifying unreported foreign bank accounts |

Sanctions for non-compliance | Civil penalties of up to $10,000-$50,000 and, in certain cases, criminal sanctions | More severe: $10,000 per violation or more; willful violations may lead to criminal proceedings and higher penalties |

Reporting party | Filed by individuals and U.S. entities such as corporations, partnerships, trusts, and estates. | Filed by individuals and by certain specified domestic entities. |

How Can You Understand What You Really Need to File?

Many taxpayers confuse FATCA and FBAR, which can lead to incomplete or incorrect filings. In practice, the first step is to determine whether the person is considered a “U.S. person” for reporting purposes. The next step is to calculate the highest balance of all foreign accounts during the year. If the aggregate amount exceeds $10,000 at any point, an FBAR must be filed, regardless of the level of income. In addition, it is necessary to check whether the foreign financial assets exceed the FATCA thresholds, based on the taxpayer’s filing status and place of residence.

It is not uncommon for a person to be required to file both reports at the same time, because they serve different legal purposes and are submitted to different authorities.

TaxLink – Our Story

Understanding the differences between FATCA and FBAR reporting obligations helps taxpayers avoid sanctions and remain on the safe side of compliance requirements.

TaxLink is a certified public accounting firm with a team specializing in both U.S. taxation and Israeli taxation. Our practical experience with the IRS and the Israel Tax Authority, together with a deep understanding of the interface between the two systems, enables us to build an end-to-end solution tailored to your specific case.

Most clients who contact us do so because they are required to file a U.S. report – whether Form 1040, FATCA reporting, FBAR filings, or reporting related to U.S. real estate investments. We manage the process as one integrated cross-border matter, with the goal of reducing errors, avoiding duplication, and helping prevent double taxation, all within the framework of U.S. law, Israeli law, and the tax treaty between Israel and the United States.

FAQ

Do you need to file both FATCA and FBAR for foreign accounts?

Sometimes. A person may be required to file both FATCA and FBAR if the relevant thresholds for each regime are met. However, these are two different sets of rules, with different categories of reporting persons, different types of assets, and different reporting thresholds.

What is the difference between the FATCA and FBAR reporting thresholds?

FATCA applies to assets above $50,000, while FBAR applies to accounts whose aggregate balance exceeds $10,000.

Is FBAR filed together with the tax return?

No. FBAR is filed separately through FinCEN’s online BSA E-Filing system and is not filed together with the federal tax return.

What happens if you do not file FBAR or FATCA?

Failure to file either report may result in significant sanctions. FBAR violations may lead to penalties of up to 50% of the account balance, while FATCA penalties start at $10,000 and may increase in the event of continued non-compliance.