In the United States, rental income can be reported in different ways, depending on how the property is used and how the rental activity is managed. Many property owners are not aware that renting out a house or apartment is not always treated as passive income. The tax implications depend on the nature of the activity and the level of the owner’s involvement.

In general, the law distinguishes between three main categories:

- regular rental activity,

- mixed use – personal use and rental use,

- and business-level hospitality that is more similar to operating a hotel. This classification is critically important because it affects not only the taxes that may apply, but also the deductions that may be claimed and whether additional U.S. tax liabilities may arise.

Deductible Expenses and Reporting (Schedule E)

When a house or apartment is rented out, the owner can generally deduct a broad range of expenses from the rental income before calculating the tax. These expenses typically include mortgage interest, property taxes, insurance, utilities, repairs, maintenance, management fees, advertising costs, and depreciation of the building over time, which can be a particularly significant deduction.

In practice, these rules are designed to ensure that tax is imposed only on the owner’s true economic profit, and not on the full amount of gross rental receipts. In most cases, the related income and expenses are reported on the taxpayer’s individual tax return using Schedule E, which is intended for rental income.

In many cases, the deductions, particularly depreciation and interest deductions, exceed the rental income in numerical terms. As a result, a tax loss may be created on paper even when the property generates positive cash flow.

Mixed-Use Residence and Personal Use

In many cases, the analysis becomes more complex when the owner also uses the property for personal purposes. An apartment or house is generally considered a personal residence if the owner, or related parties, use it for more than 14 days during the year, or for more than 10% of the number of days it is rented at fair market value, whichever is greater.

When this threshold is met, the property is classified as a mixed-use residence rather than a pure investment property. This rule applies even when the property is held primarily for investment, such as a vacation home that is rented for part of the year and used by the owner during the rest of the year.

There is also a special rule for properties rented for a very limited part of the year. If a property that is used primarily as a personal residence is rented for fewer than 15 days during the year, the rental income is generally not taken into account for federal tax purposes. In this case, the rent does not need to be reported, but expenses related to the rental also cannot be deducted. This rule generally applies when a home is rented during a major event and is intended to exempt small and occasional rentals from reporting and tax payment requirements.

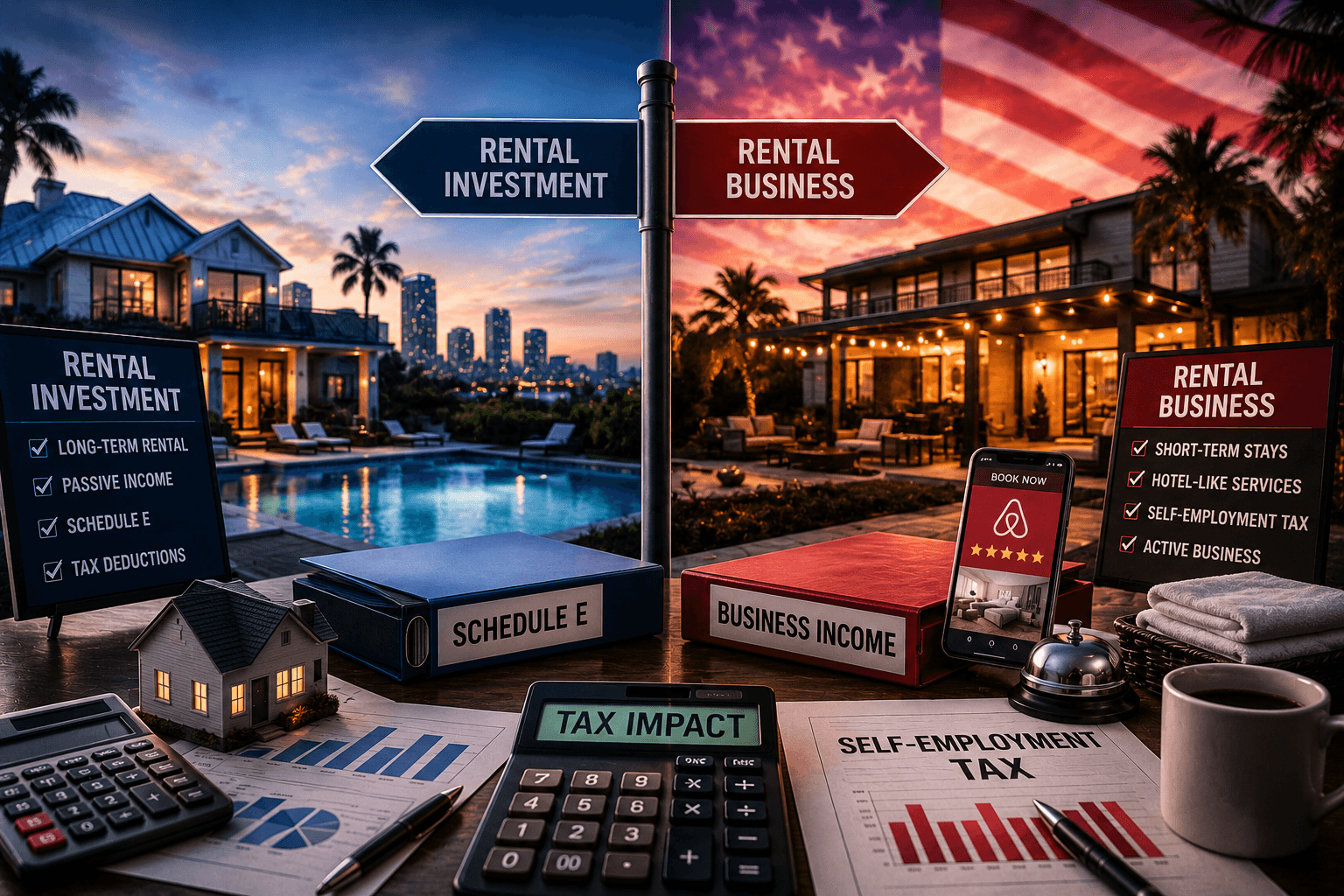

Passive Rental Activity vs. Active Business

Beyond the personal-use rules, one of the key distinctions in the U.S. taxation of rental income is between activities that are passive in nature and active activities that rise to the level of an active business. This issue usually arises in the context of short-term rentals, such as those offered through Airbnb. The determining factor is not only the length of the guest’s stay, but also the nature of the services provided, as described below.

If the owner, or a manager on the owner’s behalf, primarily provides access to the property, together with ordinary maintenance such as carrying out certain repairs to the rented property, the activity is still generally considered a rental activity, even if the rental period is short. In this case, the income is generally reported on Schedule E and is not subject to U.S. self-employment tax.

By contrast, when the rental of the property includes additional services beyond use of the property space itself, of the type generally provided by hotels, the Internal Revenue Service (IRS) may classify the activity as a hospitality business rather than as a passively held investment.

Such services may include on-site cleaning while the guest is staying at the property, providing fresh linens, check-in assistance, or ongoing responses to guests’ needs.

When the rental of a property includes additional services of this kind, the income is no longer treated as passive. Instead, it is reported as business income and may be subject to self-employment tax, in addition to regular income tax. As a result, the overall tax burden under this option may increase significantly compared with a property rented without providing additional services.

Conclusion

In summary, the U.S. tax aspects of rental property activity are not always simply a matter of collecting rent. How the property is used, whether the owner is personally present in it, the frequency of the rentals, and what additional services are provided in connection with the rental, if any, all affect the tax treatment and the deductions that may be allowed in the U.S.

U.S. tax law, like the tax laws of various countries around the world, distinguishes for purposes of taxing rental income between long-term rentals and renting out the property as a vacation home, partial Airbnb rental, or short-term rental in a hotel-style format.

In light of this, owners of U.S. real estate properties should be aware of the different tax implications arising from the different ways in which the property is used – whether as a long-term rental or for short-term activity that is more characteristic of businesses than private individuals. They should plan their steps and decisions regarding the manner of rental with awareness of the various U.S. tax implications.

Tax Link – Our Story

TaxLink is an accounting firm with a team specializing in both U.S. and Israeli taxation. Our practical experience with the Internal Revenue Service (IRS) and the Israel Tax Authority, combined with a deep understanding of the interaction between the two systems, allows us to build an end-to-end solution tailored to your case.

Most clients who contact us do so because they are required to file reports in the U.S. – whether this involves Form 1040, Foreign Account Tax Compliance Act (FATCA) reporting, Foreign Bank Account Report (FBAR) reporting, or investments in U.S. real estate. We manage the process as one coordinated cross-border matter, with the goal of reducing errors, minimizing duplication, and helping to prevent double taxation, all within the framework of U.S. law, Israeli law, and the U.S.-Israel tax treaty.

FAQ

Is every short-term rental considered a business for U.S. tax purposes?

Not necessarily. In many cases, income from a short-term rental is still considered rental income and is reported on Schedule E. The result depends largely on the services provided, and not only on the length of the stay.

Can a rental property show a tax loss even if it generates positive cash flow?

Yes. Because owners may deduct expenses such as mortgage interest, taxes, insurance, repairs, and depreciation, a property can generate positive cash flow and still show a tax loss on paper.

What happens if I also use the property personally?

Personal use can significantly change the tax treatment. Once the property crosses certain personal-use thresholds, it may be treated as a mixed-use residence rather than as a pure investment property. This may limit deductions and change the reporting method.

Why is proper classification so important for rental property owners?

Because classification affects almost everything – how the income is reported, which deductions are allowed, and whether additional taxes such as self-employment tax may apply. Proper structuring can help owners remain compliant with the law while improving tax efficiency.