U.S. Tax Refunds

Many Israelis – including U.S. citizens, real estate investors, students,

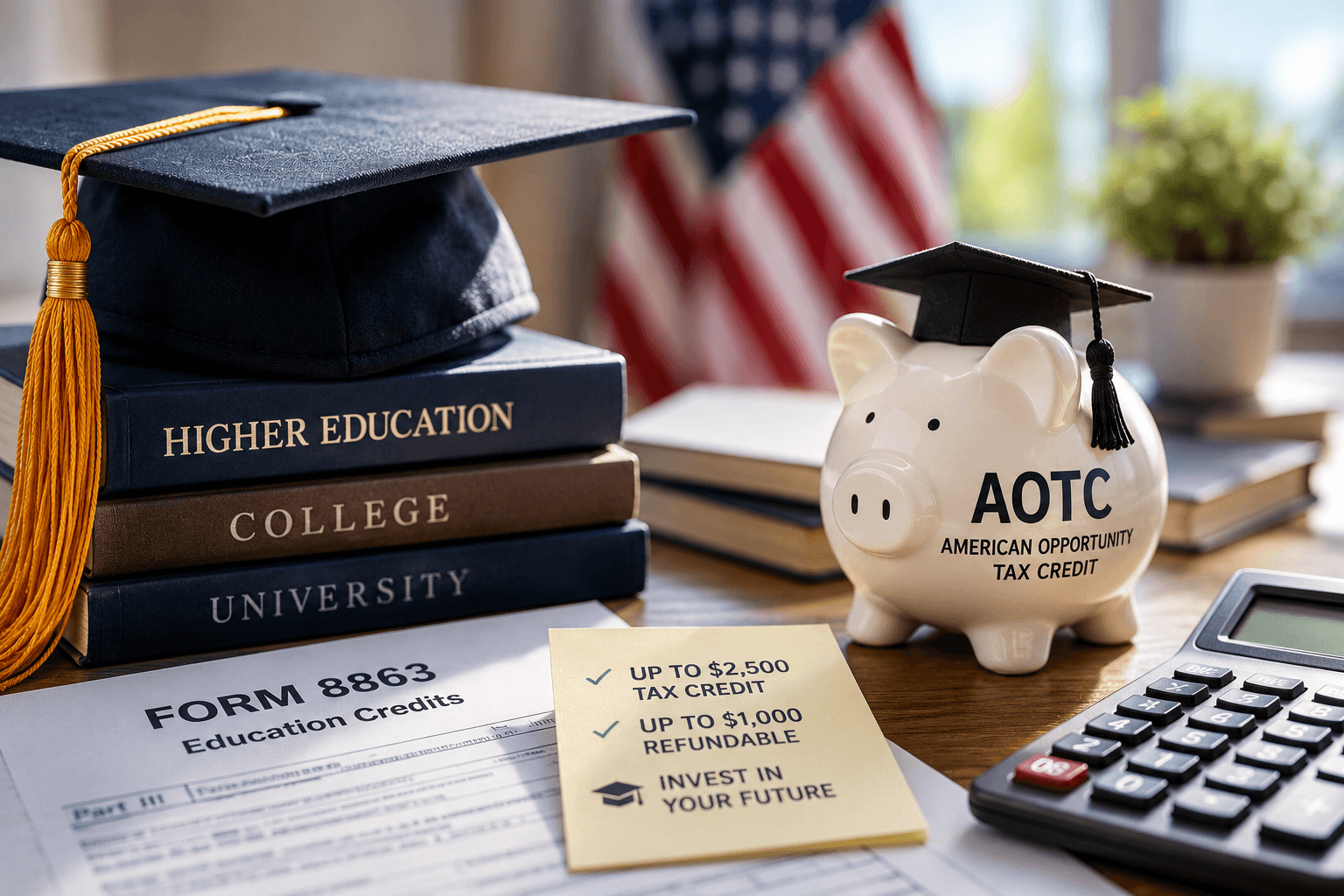

U.S. Tax Credit for Higher Education

For many students, higher education after high school is an

Taxation of Dividends Between the U.S. and Israel

If you live in Israel, hold U.S. citizenship, invest in

The Consequences of Failing to File Tax Returns in the United States

Failure to file tax returns in the United States can

Individual Taxpayer Identification Number (ITIN)

An Individual Taxpayer Identification Number (ITIN) is a tax processing

Determining Valid U.S. Tax Residency

The Tests Under U.S. Law for Determining Tax Residency for

Child Tax Credit in the U.S.

Eligibility Requirements, Benefit Amounts, and What to Know Before Filing

Taxation of Interest Income in the United States

In the United States, there are various types of investments

Tax Benefits for New Immigrants from the United States in 2026

The new temporary order opens a significant window of opportunity

Voluntary Disclosure in the US (Streamlined Procedure)

Voluntary disclosure is a framework established by the U.S. Internal Revenue Service

U.S. Filing Obligations for Green Card Holders

Pursuant to U.S. tax residency policy as outlined by the