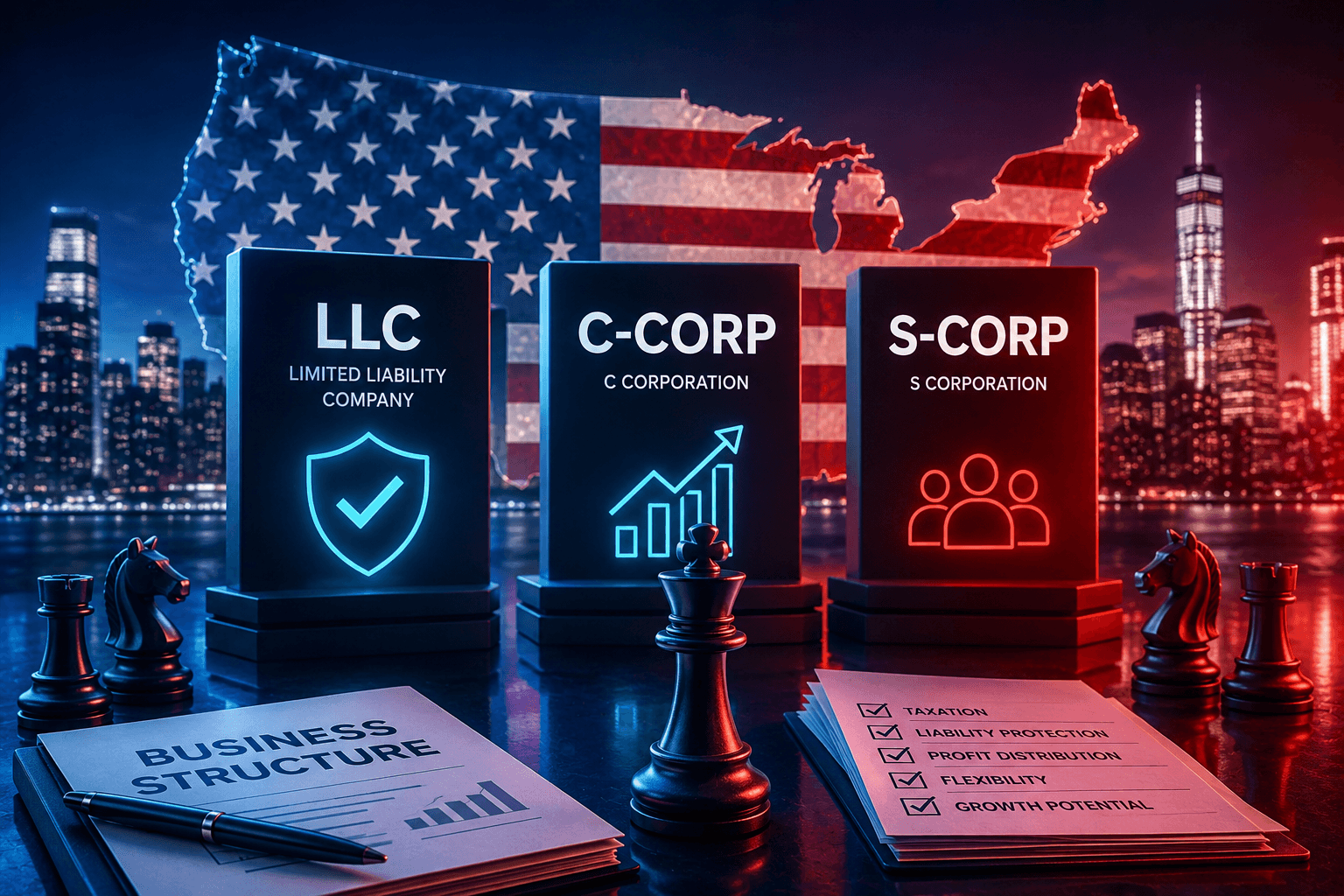

When Israeli investors or entrepreneurs consider establishing any type of business in the United States, one of the first decisions they face is which type of entity to form. The choice between a limited liability company (LLC), a C Corporation (C-Corp), or an S Corporation (S-Corp) affects, among other things, how the business is taxed and how profits are distributed.

These differences are especially important for Israeli residents who are not U.S. citizens and are not U.S. tax residents, since not every structure is suitable for foreign owners in the United States

LLC

An LLC is one of the most flexible and commonly used business structures in the United States. It is formed under the laws of the relevant state and combines limited liability protection with tax flexibility. An LLC may be owned by individuals, partnerships, corporations, or even other LLCs, with relatively few ownership restrictions.

An LLC is generally treated as a “pass-through entity” for tax purposes, meaning that profits and losses “pass through” to the owners and are reported on their personal tax returns, while the entity itself does not pay federal income tax.

Put simply, the LLC itself does not pay federal income tax in the United States, and LLC members who are not U.S. residents are taxed only on U.S.-source income.

C-Corp

Unlike an LLC, a C-Corp is a traditional corporation under U.S. law. It is legally separate from its owners and may offer advantages when raising outside investment.

C-Corps pay corporate income tax at a flat federal rate (as of 2026, 21%). When profits are distributed to shareholders as dividends, those dividends may be taxed again at the shareholder level under what is commonly known as a “double taxation” model. This means the company pays tax on its income, and dividend distributions may then be subject to U.S. withholding tax at a rate of 30%, unless a reduced rate applies under a relevant tax treaty, such as the tax treaty between the United States and Israel.

These entities are well suited to a business model in which the investor intends to retain profits in the business for growth, attract outside investors, or use stock-based compensation for employees. This is because the share structure of a C-Corp allows for stock options and similar incentives for employees, whereas providing this type of incentive is more complex in an LLC structure.

S-Corp

An S-Corp combines characteristics of both a C-Corp and an LLC.

From a legal perspective, it operates as a corporation, but for tax purposes it is treated similarly to an LLC. In other words, LLC, S-Corp generally is not subject to federal income tax at the entity level. Instead, profits and losses are allocated directly to the shareholders (or members, where the entity is LLC), who report them on their personal tax returns.

In addition, every S-Corp must pay its owners or shareholders a reasonable salary, and it may also make dividend distributions, subject to Internal Revenue Service (IRS) requirements.

Because S-Corp allocates income directly to its owners and generally does not pay federal income tax at the entity level, it may offer significant tax advantages to small businesses, including a lower overall tax burden.

However, S-Corp status comes with unique limitations, including:

- No more than 100 shareholders;

- Only U.S. citizens or U.S. tax residents may be shareholders;

- Only one class of stock is permitted.

Profit Distribution and Risk Management

The following table provides a comparative summary of the differences among the three business structures in terms of profit distribution and legal protection against claims:

Business Structure | Profit Distribution | Liability Protection |

LLC | Profits are allocated directly to the owners and reported on their personal tax returns. Distributions are flexible and are not subject to dividend distribution rules | Limited liability protection. Owners generally are not personally liable for the company’s debts or claims against it |

C-Corporation | Profits are taxed at the company level. When profits are distributed as dividends, shareholders are taxed again at the personal level | Strong liability protection. Shareholders’ personal assets are generally protected from the company’s liabilities and claims |

S-Corporation | Profits are allocated to shareholders and reported on their personal tax returns | Limited liability protection, similar to a C-Corp |

Considerations Relating to Foreign Ownership

For Israeli investors seeking to enter the U.S. market, choosing the right business structure is a material decision with commercial, legal, and tax implications. While each of these three structures offers certain advantages, the differences among them may directly affect the way the business operates, its ability to raise capital, how profits are distributed, and of course the overall tax burden.

Accordingly, the choice of entity structure should be made only after reviewing all relevant factors, including the nature of the business, where income will be generated, the identity of the shareholders or members, the expected number of investors, the need to raise outside capital, whether the goal is to distribute funds to the owners or retain profits in the company for growth, the complexity of ongoing U.S. reporting, withholding tax considerations, possible implications under Israeli tax law, and considerations relating to a future exit or restructuring.

For many Israeli investors establishing business activity in the United States, an LLC is often a practical and convenient option, mainly because it may offer operational flexibility, relative simplicity, and a better fit where flexibility is needed or where a more rigid corporate framework is not required.

By contrast, if the goal is growth, raising investment, or reinvesting profits for the long term, a C-Corp may be better suited to achieve those objectives. An S-Corp, on the other hand, may be preferable to a C-Corp in certain cases, but this option is generally not available to non-U.S. owners. This is because U.S. tax law imposes restrictions on who may hold shares in an S-Corporation, and in most cases only U.S. persons may do so. Therefore, an Israeli investor who is not a U.S. citizen or a U.S. tax resident generally cannot hold an interest in an S-Corp directly.

TaxLink – Our Story

Our team focuses on U.S. taxation for Israeli investors and can help you choose the right structure, while also guiding you through the formation process and the various tax issues that may accompany these investments.

TaxLink is a certified public accounting firm with a team specializing in both U.S. and Israeli taxation. Our hands-on experience with the IRS and the Israel Tax Authority, together with a deep understanding of the interaction between the two systems, allows us to build an end-to-end solution tailored to your specific case. Our team focuses on U.S. taxation for Israeli investors and can help you choose the right structure, while also guiding you through the formation process and the related tax framework.

Most clients who come to us do so because they are required to file reports in the United States, whether this involves Form 1040, Foreign Account Tax Compliance Act (FATCA) reporting, Foreign Bank Account Report (FBAR) filings, or U.S. real estate investments. We manage the process as one coordinated cross-border matter, with the goal of reducing errors, minimizing duplication, and helping prevent double taxation, all within the framework of U.S. law, Israeli law, and the tax treaty between the United States and Israel.

FAQs

Can an Israeli citizen own an S corporation?

An S corporation generally cannot have shareholders who are foreign individuals and are not U.S. tax residents. An Israeli citizen may qualify only if he or she is considered a U.S. tax resident and meets the eligibility rules applicable to an S-Corp.

Is an LLC always a pass-through for U.S. tax purposes?

No. The default tax classification of an LLC depends on the number of members it has. It may also elect to be taxed as a corporation.

Which structure is generally preferable for raising venture capital?

Many investors prefer C corporations for equity investments and stock-based incentives, but the right choice depends on your specific circumstances and objectives.

What filings are foreign-owned U.S. entities expected to submit?

Foreign ownership may trigger additional U.S. filing obligations and withholding tax requirements. Early compliance planning can help prevent tax penalties.